|

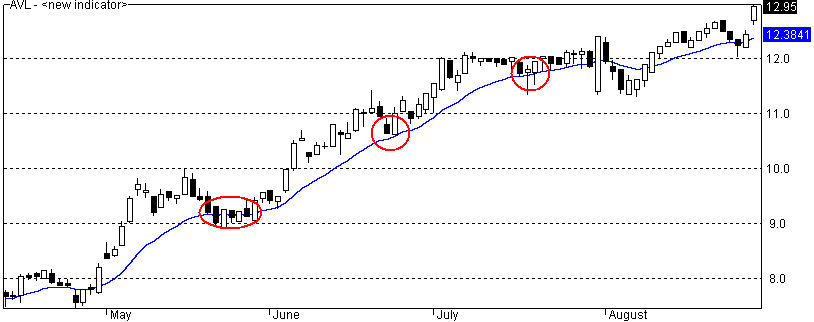

In our last article we discussed how we can profit from an exponential moving average. Today we will learn how to determine the optimal length of a moving average. This is critical if we are to get profitable results. Last time we looked at an example of AVL with an exponential moving average (ema) and saw an opportunity for some long positions. Here is the chart we looked at with the exponential moving averagein blue and the long entry opportunities circled in red;

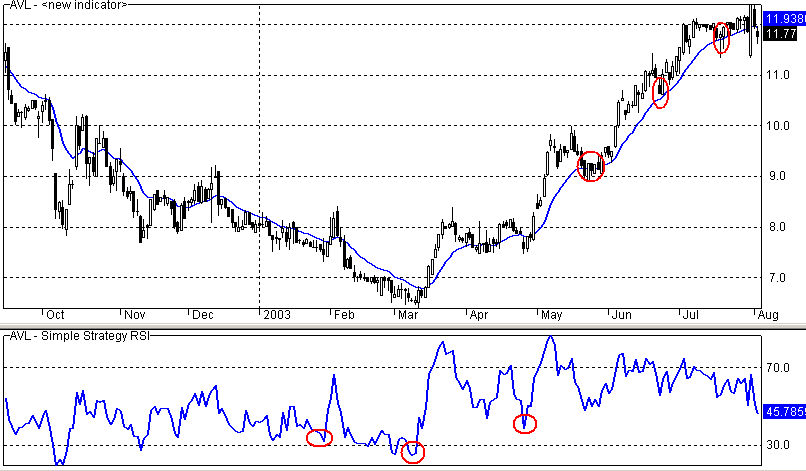

As you can see, two of the three would have been great long positions for swing trades. So what length did I choose for the exponential moving averageand how did I choose it? That's the one million dollar question! If we choose a length that is too short, the line will run so close to the price that it will never appear to break away from it. If we choose a length that is too long, the price will never come close enough to it to invite us to open a trade. The key to finding this "ideal" exponential moving average length is to remove the noise of the market. This is not an exact science, but an effective way to do so is to remove the dominant cycle of the price movement. If we lay out an ema that doesn't take into account the dominant cycle (major swings) of the price, then it will become more useful to us. We do this by using an ema that is 1/2 the dominant cylcle of the price movement. Now some will argue that "real mathematical cycles" seldom exist in market movement. That may be true, but more often than not there exists a rhythm in the movement of the price, and it will suffice for this purpose. So how do we determine what the dominant cycle is? There is more than one way of doing this and depending upon who you ask, you may get different answers as to which way is best. A simple and quick way of doing this (something most of us are interested in) is to use an RSI chart. Simply look for the significant dips in the RSI. I usually count the last three from the current point on the chart. Count the distance between the first and second, then between the second and third and average the two. Lets see how this worked out for the example of AVL by adding the RSI, and a little history to our chart below;

So we can see in the above example, when we back up from our point of interest at the beginning of June that there are major or significant lows in the RSI chart, late in April, then early in March and third, late in January. I counted 33 days between the April and March dip, and 26 between the March and January dip for a total of 59 days. Divide that by 2 and you get an average dominant cycle of 29.5 days. We then further divide that number by 2 to come up with 1/2 of the dominant cycle which is 15, and that is the magic number we come up with for our exponential moving average in this example. How long can we use the 15 day exponential moving average for? As a general rule you should at least be able to use it for the length of the current dominate cycle that has been identified. The further away you get from that point, you might want to think about recalculating. If this information is new to you or you would like to learn about other profitable trading tips and resources, simply enter your name and email address below and we'll be glad to share them with you.

All email addresses are kept confidential and are never shared with anyone.

KNOWLEDGE IS POWER

Terms and Conditions / Risk Disclosure

Copyright 2006, All Rights Reserved

|